Real Exam Questions and Answers as experienced in Test Center

BEC Braindumps with 100% Guaranteed Actual Questions | https:alphernet.com.au

BEC practice questions - CPA Business Environment and Concepts Updated: 2024 | ||||||||

| Free killexams.com BEC question bank | ||||||||

|

||||||||

|

||||||||

|

Exam Code: BEC CPA Business Environment and Concepts practice questions January 2024 by Killexams.com team | ||||||||

BEC CPA Business Environment and Concepts Business Environment and concept section is treated as one of the most challenging exams because of its extensive material and it deals with business and economic concepts. The CPA BEC section will help you to move one step further in business knowledge and help them apply the knowledge in real-world scenarios. Business Environment and concepts covers: Business environment in general, and its core concepts. Foundational grounding in accounting and are exposed to underlying reasons for accounting implications Financial management information technology, and business strategies in addition to accounting concepts. Economic concepts, financial management, information systems and communications, strategic planning and operations management. Testing to determine different business strategies with their knowledge in strategic planning and market risks. Making financial decisions, forecasting trends in the market, and understanding internets implication in business. Topic Percentage Corporate Governance 16% – 20% Economic Concepts and Analysis 16% – 20% Financial Management 19% – 23% Information Systems and Communications 15% – 19% Strategic Planning 10% – 14% Operations Management 12% – 16% BEC1 Business Environment and Concepts (BEC) BEC2 Section introduction BEC6 Summary blueprint BEC7 Area I — Corporate Governance BEC9 Area II — Economic Concepts and Analysis BEC11 Area III — Financial Management BEC13 Area IV — Information Technology BEC16 Area V — Operations Management The Business Environment and Concepts (BEC) section of the Uniform CPA Examination (the Exam) tests knowledge and skills that a newly licensed CPA must demonstrate when performing: • Audit, attest, accounting and review services • Financial reporting • Tax preparation • Other professional responsibilities in their role as certified public accountants The content areas tested under the BEC section of the test encompass five diverse subject areas. These content areas are corporate governance, economic concepts and analysis, financial management, information technology and operations management. Reference materials relevant to the BEC section of the Exam are included under References at the conclusion of this introduction. Content organization and tasks The BEC section blueprint is organized by content AREA, content GROUP and content TOPIC. Each group or course includes one or more representative TASKS that a newly licensed CPA may be expected to complete when performing audit, attest, accounting and review services, financial reporting, tax preparation or other professional responsibilities. The tasks in the blueprint are representative. They are not intended to be (nor should they be viewed as) an all-inclusive list of tasks that may be tested in the BEC section of the Exam. Additionally, it should be noted that the number of tasks associated with a particular content group or course is not indicative of the extent such content group, course or related skill level will be assessed on the Exam. Similarly, examples provided within the task statements should not be viewed as all-inclusive. Area II of the BEC section blueprint covers several subjects related to Economic Concepts and Analysis, including the following: • Knowledge of economic concepts and analysis that would demonstrate an understanding of the impact of business cycles on an entitys industry or business operation • Determining market influences on the business environment, such as globalization • Determining the business reasons for, and the underlying economic substance of, transactions and their accounting implications • Understanding financial risks and the methods for mitigating the impact of these risks Area III of the BEC section blueprint covers several subjects related to Financial Management, including the following: • Assessing the factors influencing a companys capital structure, such as risk, leverage, cost of capital, growth rate, profitability, asset structure and loan covenants • Calculating metrics associated with the components of working capital, such as current ratio, quick ratio, cash conversion cycle, turnover ratios • Determining the impact of business decisions on working capital • Understanding commonly used financial valuation and decision models and applying that knowledge to assess assumptions, calculate the value of assets and compare investment alternatives Area IV of the BEC section blueprint covers several subjects related to Information Technology (IT), including the following: • Understanding the role of IT and systems, including the use of data in supporting business decisions. • Identifying IT-related risks associated with an entitys information systems and processes, such as processing integrity, protection of information and system availability, including those risks introduced by the relationships with third-parties. • Identifying application and IT general control activities, whether manual, IT dependent or automated, that are responsive to IT-related risks, such as access and authorization controls, system implementation testing and incident response plans. Area V of the BEC section blueprint covers several subjects related to Operations Management, including the following: • Understanding business operations and use of quality control initiatives and performance measures to Boost operations • Application of cost accounting concepts and use of variance analysis techniques • Utilizing budgeting and forecasting techniques to monitor progress and enhance accountability The test focuses on testing higher order skills. Based on the nature of the task, each representative task in the BEC section blueprint is assigned a skill level. BEC section considerations related to the skill levels are discussed below. • Remembering and Understanding is tested in all five areas of the BEC section. Remembering and understanding tasks focus on the knowledge necessary to demonstrate an understanding of the general business environment and business concepts, such as those involving enterprise risk management. • Application is also tested in all five areas of the BEC section. Application tasks focus on general subjects such as those found in the subjects of economics and information technology, and the day-to-day financial management tasks that newly licensed CPAs perform, such as those involving calculations involving ratios, valuation and budgeting. • Analysis skills, tested in Areas II, III and V involve tasks that require a higher level of analysis and interpretation. These tasks, such as comparing investment alternatives using calculations of financial metrics, financial modeling, forecasting and projection, frequently require newly licensed CPAs to gather evidence to support inferences. The representative tasks combine both the applicable content knowledge and the skills required in the context of the work that a newly licensed CPA would reasonably be expected to perform. The BEC section does not test any content at the Evaluation skill level as newly licensed CPAs are not expected to demonstrate that level of skill in regards to the BEC content. References — Business Environment and Concepts • The Committee of Sponsoring Organizations of the Treadway Commission (COSO): – Internal Control – Integrated Framework – Enterprise Risk Management – Integrating with Strategy and Performance – COSO-issued application material, thought papers and guides related to the above frameworks • Sarbanes-Oxley Act of 2002: – Title III, Corporate Responsibility – Title IV, Enhanced Financial Disclosures – Title VIII, Corporate and Criminal Fraud Accountability – Title IX, White-Collar Crime Penalty Enhancements – Title XI, Corporate Fraud Accountability • Current business periodicals • Current textbooks on: – Accounting Information Systems – Budgeting and Measurement – Corporate Governance – Economics – Enterprise Risk Management – Finance – Management – Management Information Systems – Managerial Accounting – Production Operations | ||||||||

| CPA Business Environment and Concepts AICPA Environment Practice Test | ||||||||

Other AICPA examsBEC CPA Business Environment and ConceptsFAR CPA Financial Accounting and Reporting CPA-REG CPA Regulation CPA-AUD CPA Auditing and Attestation PCAP-31-03 Certified Associate in Python Programming - 2023 PCEP-30-01 Certified Entry-Level Python Programmer | ||||||||

| killexams.com includes latest and updated BEC practice questions with genuine BEC test mock test for new syllabus. Practice their Real BEC Questions and BEC braindumps to Boost your insight and pass your test with High Marks. They guarantee your achievement in the exam, covering every one of the points of exam. Pass4sure beyond any doubt with their exact questions. | ||||||||

| AICPA BEC CPA Business Environment and Concepts https://killexams.com/pass4sure/exam-detail/BEC Question: 245 The imputed interest rate used in the residual income approach to performance evaluation can best be described as the: A. Historical weighted average cost of capital for the company. B. Target return on investment set by the company's management. C. Average return on investments for the company over the last several years. D. Marginal after-tax cost of capital on new equity capital. Answer: B Explanation: Choice "b" is correct. The imputed interest rate used in the residual income approach can best be described as the target return on investment set by the company's management. Choice "a" is incorrect, but it is a close second. The historical weighted average cost of capital may be how management sets the target return on investment. Choice "c" is incorrect. The average return on investments for past years may not be a good indication of management's future intentions. Choice "d" is incorrect. Marginal after-tax cost of capital on new equity may be how management sets its targets, but it may not be, too. Question: 246 One approach to measuring divisional performance is return on investment. Return on investment is expressed as operating income: A. Divided by the current year's capital expenditures plus cost of capital. B. Divided by fixed assets. C. Divided by current assets. D. Divided by total assets. Answer: D Explanation: Choice "d" is correct. Return on investment is operating income divided by total assets. Choice "a" is incorrect. Current year's capital expenditures plus cost of capital would be a meaningless denominator. Choice "b" is incorrect. This omits the current assets employed by the division. Choice "c" is incorrect. This omits fixed assets. Question: 247 The following selected data pertain to the Darwin Division of Beagle Co. for 1994: What was Darwin's 1994 residual income? A. $0 B. $4,000 C. $10,000 D. $30,000 Answer: D Explanation: Choice "d" is correct. Residual income is income less the imputed interest rate times average invested capital. Capital turnover is equal to sales / average invested capital. Choice "a" is incorrect. Residual income is greater than zero. The imputed interest rate times average invested capital needs to be compared with operating income. Choice "b" is incorrect. Residual income is not simply the imputed interest rate times operating income. The imputed interest rate times average invested capital needs to be compared with operating income. Choice "c" is incorrect. Residual income is not simply imputed interest rate times average invested capital. The operating income must be considered. Question: 248 Select Co. had the following 1994 financial statement relationships: Asset turnover 5 Profit margin on sales 0.02 What was Select's 1994 percentage return on assets? A. 0.1 percent. B. 0.4 percent. C. 2.5 percent. D. 10.0 percent. Answer: D Explanation: Choice "d" is correct. Return on assets equals income divided by average assets. This formula can be further divided into the components of profit margin times asset turnover (referred to as the Dupont formula): Choices "a", "b", and "c" are incorrect, per the above calculation. Question: 249 The following information pertains to Quest Co.'s Gold Division for 1993: Quest's return on investment was: A. 10.00 percent. B. 13.33 percent. C. 27.50 percent. D. 30.00 percent. Answer: C Explanation: Choice "c" is correct. Return on investment equals net income divided by average invested capital: Choices "a", "b", and "d" are incorrect, per the above calculation. Question: 250 Williams, Inc. is interested in measuring its overall cost of capital and has gathered the following data. Under the terms described below, the company can sell unlimited amounts of all instruments. . Williams can raise cash by selling $1,000, 8 percent, 20-year bonds with annual interest payments. In selling the issue, an average premium of $30 per bond would be received, and the firm must pay floatation costs of $30 per bond. The after-tax cost of funds is estimated to be 4.8 percent. . Williams can sell 8 percent preferred stock at par value, $105 per share. The cost of issuing and selling the preferred stock is expected to be $5 per share. . Williams' common stock is currently selling for $100 per share. The firm expects to pay cash dividends of $7 per share next year, and the dividends are expected to remain constant. The stock will have to be underpriced by $3 per share, and floatation costs are expected to amount to $5 per share. . Williams expects to have available $100,000 of retained earnings in the coming year; once these retained earnings are exhausted, the firm will use new common stock as the form of common stock equity financing. . Williams' preferred capital structure is: Long-term debt 30% Preferred stock 20 Common stock 50 The cost of funds from retained earnings for Williams, Inc. is: A. 7.0 percent. B. 7.4 percent. C. 8.1 percent. D. 7.8 percent. Answer: A Explanation: Choice "a" is correct. 7.0 percent cost of funds from retained earnings. The cost of retained earnings is equal to the rate of return required by the firm's common shareholders (or, in effect, the return "lost" by them when the firm chooses to fund with retained earnings). While oftentimes this rate is somewhat subjective, they are given the facts to exactly answer the question in this case. The stock is currently selling for $100/share, and the dividend is given at $7/share. $7 / $100 = 7% Choices "b", "c", and "d" are incorrect, per the above Explanation:/calculation. For More exams visit https://killexams.com/vendors-exam-list Kill your test at First Attempt....Guaranteed! | ||||||||

|

Being prepared is the best way to ease the stress of test taking. If you are having difficulty scheduling your Placement Test, please contact the UNG Testing Office. If you have a red yes in any Placement Test Required row on your Check Application Status page in Banner, read the information below relating to the area in which you have the red yes. Establishing Connection... Samantha Bowling, CPA, CGMA, knows a thing or two about how accounting firms can use technology to boost audit quality. As managing partner at Upper Marlboro, Md.-based Garbelman Winslow CPAs, Bowling spearheaded the firm’s implementation of artificial intelligence (AI) to identify high-risk transactions. As chair of the AICPA Auditing Standards Board (ASB) Technology Task Force, Bowling leads a group of volunteers dedicated to developing examples of how to use technology to transform audit processes, resulting in higher quality audits. “It’s about transforming what you do to be more effective and eventually more efficient,” said Bowling, whose firm has been recognized as a leader in AI usage despite having fewer than 20 employees. “You should not adopt technology to do the same process you did last year faster. The efficiency happens when you transform how you audit and elevate your team to a higher level of thinking.” This article, the first in a four-part series (see the box “Looking Ahead” at the end of this article), identifies the incentives for using technology in an audit. The article also provides findings from an ASB survey on the impediments to technology use in audits, one of many steps the ASB has taken to understand and support technology transformation of the audit. TRANSFORMING THE AUDIT In the latest past, the typical delivery of the audit was document-checklist driven. Cloud and other technologies, notably AI and data analytics, have allowed for the audit to be delivered more efficiently and effectively. Today, auditors are moving into the next stage of audit transformation, as shown in the graphic “AICPA/CPA.com Audit Transformation Maturity Model” (below). There will be further advances — and deeper insight into engagements — as auditors embrace fully integrated, knowledge-driven approaches that are technology-enabled through AI and other technologies.

At the same time, a latest practice aid from the ASB’s Technology Task Force, “Use of Technology in an Audit of Financial Statements,” helps auditors with tailoring their risk assessment. The practice aid describes and illustrates through examples how technology can Boost audit effectiveness and efficiency, with an initial focus on the risk identification and assessment process under Statement on Auditing Standards (SAS) No. 145, Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement. IMPROVING PLANNING AND PROCESSES SAS No. 145 requires firms to gain an understanding of the entity’s use of technology relevant to the preparation of the financial statements, and it has a direct impact on how they plan the audit by tailoring audit programs and designing audit procedures that are responsive to the assessed risk, Bowling said. For example, when a client adopts a new technology, firms can’t just repeat past audit processes because they may no longer be appropriate. Instead, firms need to know technologies well enough to see how they affect client workflow and then adjust audit procedures accordingly. In this way, SAS No. 145 opens opportunities for auditors to use technology to analyze data and transform how they audit. Bowling, for instance, finds AI to be a valuable tool in the planning and initial risk assessment stage of the audit. Whereas some auditors may plan and conduct initial risk assessments using traditional techniques (checklists and minimal technology use), AI analyzes risk in client data and provides Bowling with insights she uses to refine her audit plan for each client. The ability to more specifically identify risk allows auditors to develop procedures to target those risks rather than perform generic audit procedures that may be more time-consuming and costly and aren’t calibrated for high-risk areas. AI technology can also Boost information-gathering capability, especially in complex audits, according to Patricia Willhite, CPA, senior audit manager at CapinCrouse, a 200-employee firm that specializes in serving not-for-profits. “A process improvement can make us faster and reduce the time they spend,” Willhite said. With her government clients in particular, technology-driven efficiencies can make it easier to monitor and address new rules as they are added in this highly regulated field. HOW STAFFING IS AFFECTED AI technology can help newer staff members develop a keener eye while augmenting their existing knowledge, Bowling said. For example, not only can the technology take over much of the work of choosing sample selections, it can also allow staff to learn from the software by seeing what control points are triggered when the technology highlights a high-risk transaction. “Using the software provides the ‘why’ behind the audit process,” she said. And when firms support a staff member in their role as the technology-innovation champion with appropriate compensation and the ability to celebrate successes and failure, they will reap the benefits, according to Bowling. “A culture of innovation and fixing what is broken generates a contagious enthusiasm among staff for change,” she said. At the 220-employee firm Smith and Howard in Atlanta, one audit senior manager with an interest in technology has become the internal IT expert, with the firm supporting her efforts by reducing her billable hours requirement. “Many firms have someone who can take on this role,” said Sean Spitzer, CPA, the firm’s president, “but you have to give them the time and space to do it.” SURVEY: BARRIERS TO TECHNOLOGY USE The ASB survey conducted late last year sought to identify barriers that prevent auditors from making use of IT, including emerging technologies. Nearly 60% of respondents came from firms with 50 or fewer professionals; of these, almost half came from firms with fewer than 10. In designing the survey, a key question for the ASB was whether auditors believed that U.S. generally accepted auditing standards (GAAS) hindered their use of technology in an audit. As the chart “What Limits Technology Use?” (below) shows, few respondents identified GAAS as a stumbling block. While impediments varied by technology type, respondents named the following as the most common hurdles:

The survey revealed several tiers of technology use. Most respondents were using cloud technology, mainly for planning, audit documentation, journal-entry testing, confirmations, and tests of details as well as collaboration and information-sharing. Data analytics and data visualization were the next most often used technologies, with data analytics put to work in journal-entry testing and data visualization used mostly for planning, risk assessment, audit documentation, and substantive analytical procedures. AI and textual analysis were employed generally for journal-entry testing and audit documentation, respectively, but they were (like some other technologies) infrequently used. A total of 17% of respondents reported using no emerging technology included in the survey. Overall, the survey results suggest there are opportunities for firms to use emerging technologies on audit engagements and strategies that firms can implement to overcome barriers in technology use. As the profession embraces emerging technology and technology transformation, CPAs are adapting new ways to conduct their audits. Looking ahead Forthcoming articles in this four-part series will cover the following topics:

About the authors Anita Dennis is a New Jersey-based freelance writer. J. Gregory Jenkins, CPA, Ph.D., is the Ingwersen Professor in the School of Accountancy in the Harbert College of Business at Auburn University. To comment on this article or to suggest an idea for another article, contact Jeff Drew at Jeff.Drew@aicpa-cima.com. AICPA & CIMA RESOURCES Articles “How 3 Firms Tackle the Audit Talent Crunch,” JofA, Sept. 1, 2023 “An Updated Practice Aid and How It Can Assist in Audits of Digital Assets,” JofA, Aug. 31, 2023 “AICPA Debuts New Practice Aid for Tech-Enabled Auditing,” JofA, July 27, 2023 “5 Ways Firms Can Use Technology to Transform Audits,” JofA, Dec. 20, 2022 Tool Enhance your risk assessment procedures with the use of automated tools and techniques in the auditor’s risk assessment. CPA.com insights and research Leverage cutting-edge tools and technology to modernize your A&A practice. For more information or to make a purchase, go to aicpa-cima.com/cpe-learning or call 888-777-7077. Crossref Citations This Book has been cited by the following publications. This list is generated based on data provided by Crossref.2019. Highlights of latest Book Publications (August 2018 to July 2019). Transnational Environmental Law, Vol. 8, Issue. 3, p. 589. 2019. Books Received. American Journal of International Law, Vol. 113, Issue. 3, p. 674. Follesdal, Andreas 2020. Survey Article: The Legitimacy of International Courts*. Journal of Political Philosophy, Vol. 28, Issue. 4, p. 476. Voigt, Christina 2021. International Environmental Responsibility and Liability. SSRN Electronic Journal , Pihl, Erik Alfredsson, Eva Bengtsson, Magnus Bowen, Kathryn J. Cástan Broto, Vanesa Chou, Kuei Tien Cleugh, Helen Ebi, Kristie Edwards, Clea M. Fisher, Eleanor Friedlingstein, Pierre Godoy-Faúndez, Alex Gupta, Mukesh Harrington, Alexandra R. Hayes, Katie Hayward, Bronwyn M. Hebden, Sophie R. Hickmann, Thomas Hugelius, Gustaf Ilyina, Tatiana Jackson, Robert B. Keenan, Trevor F. Lambino, Ria A. Leuzinger, Sebastian Malmaeus, Mikael McDonald, Robert I. McMichael, Celia Miller, Clark A. Muratori, Matteo Nagabhatla, Nidhi Nagendra, Harini Passarello, Cristian Penuelas, Josep Pongratz, Julia Rockström, Johan Romero-Lankao, Patricia Roy, Joyashree Scaife, Adam A. Schlosser, Peter Schuur, Edward Scobie, Michelle Sherwood, Steven C. Sioen, Giles B. Skovgaard, Jakob Sobenes Obregon, Edgardo A. Sonntag, Sebastian Spangenberg, Joachim H. Spijkers, Otto Srivastava, Leena Stammer, Detlef B. Torres, Pedro H. C. Turetsky, Merritt R. Ukkola, Anna M. van Vuuren, Detlef P. Voigt, Christina Wannous, Chadia and Zelinka, Mark D. 2021. Ten new insights in climate science 2020 – a horizon scan. Global Sustainability, Vol. 4, Issue. , Song, Yan 2022. The Obligation of EIA in the International Jurisprudence and Its Impact on the BBNJ Negotiations. Sustainability, Vol. 15, Issue. 1, p. 487.

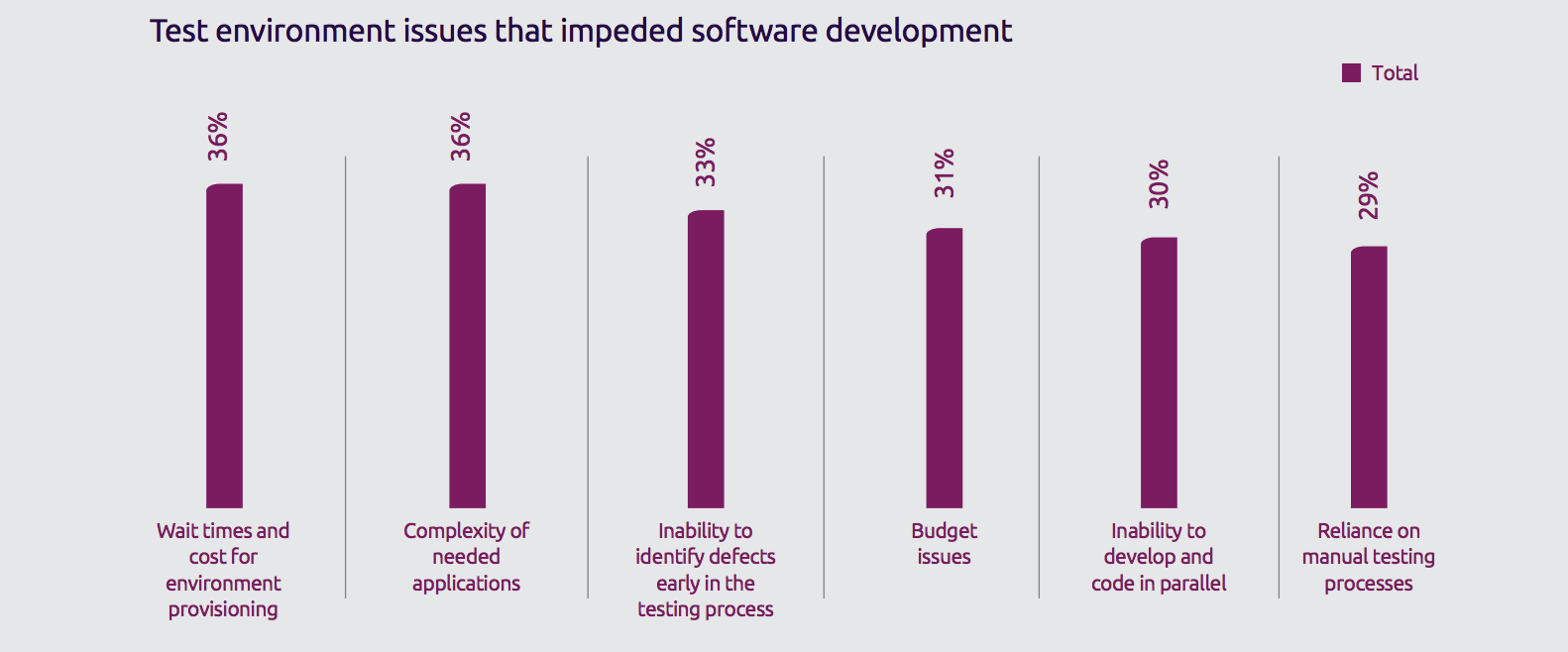

Companies have heard the saying “test early and test often” more times than they can count, but in a DevOps environment, testing is an important aspect of the software development process. SD Times spoke with some experts about how much testing can be done in a Dev-Test-Ops environment, and how companies can determine how much testing is enough. Matthew Brayley-Berger, worldwide product marketing manager at HPE The majority of organizations undertake a continuous release strategy to provide faster support for the business, so it makes sense that quality needs to be an important consideration. It doesn’t take many high-severity defects or late-stage integration issues to undo any speed gained, and that’s kind of the point. Teams need to have a holistic view of how quality is measured and what likely vulnerabilities…exist so that they can deliberately plan a remediation strategy. Such strategies could include planning higher levels of core-architectural automated testing, or ensuring that end users are available earlier in the process. The key in any Continuous Delivery environment is to shrink the gap between integrations and tests, to ensure that any corrective action is minimal and consumable within the team’s velocity. Many larger organizations struggle with what they call “a hardening sprint,” and if that works for the organization’s timelines/business needs, there isn’t an issue. But for many organizations, this is your early warning sign that the team is taking on too much work, or aren’t sufficiently validating quality. So how much testing is enough? It does depend, but I always like to recommend that organizations have a solid life-cycle management platform to help them better scope what needs to be tested, and to deliberately have people on the team focused on architecting and validating “quality” throughout the release. Testers, I argue, absolutely do exist in an agile world, and they have a critical part on any team by helping everyone to catch errors and validate core business capability as early as possible. In fact, it’s these testers—QA professionals—working as a part of the core team that can help ensure that they are testing enough, thinking about and building automation, and help course-correct early in the life cycle, when warning signs begin to emerge. The other secret that I’ve seen really help teams, with respect to quality, is using service virtualization to help ensure that they can actually test earlier and more frequently. I’ve seen far too many high-velocity teams fall prey to broken dependent services, or infrastructure issues (e.g. access to a mainframe). In this day in age, virtualization is such a no-brainer, there really isn’t an excuse for not using it. Dan McFall, vice president of mobility solutions at Mobile Labs On the other hand, customers have functionality expectations you must meet, and you cannot always get a second chance. As a minimum in a Dev-Test-Ops world, you should have a full regression suite ready to run before each release. Then you need to understand the interoperability and non-functional components of the application as well. Performance and UX are also crucial, but if you have solid monitoring and feedback processes, these can be handled in production if you are committed to rapid responses. Ultimately, more testing is always better than less. The more testing, results and correction processes you can automate, the better off you will be. Just don’t forget that part of the reason for Dev-Test-Ops is to get new code out the door. It can still be tempting to naval gaze, but then you might as well go back to waterfall development. Jason Hammon, director of product management at TechExcel Test-management solutions make it easier to determine what coverage has been completed and what areas still need to be tested. When test management includes, or is integrated with, requirements management, test teams can also ensure that all of the requirements have been successfully tested, ensuring that each delivery matches expectations. While a Dev-Test-Ops environment can present challenges for testing teams, careful planning and execution tracking will still lead to successful deliveries. Tom Lounibos, CEO of SOASTA When the production system is not an exact match of the pre-prod system, the load tests aren’t a reliable measure for production, nor what performance can be expected. This is due to the differences between prod and pre-prod, including network, load balancers, firewall, plus any server configuration differences. Testing the production system is the only reliable way to measure the performance it will deliver under load. Waiting to test in production is too late. A performance baseline must be set in development, where poor-performing code is not promoted into the release. Some engineering teams already use tools like JMeter to load test in development. Adding performance testing into the Continuous Integration system institutionalizes these tests. While performance testing moves left, functional testing also moves right into production, where the application is Tested not only to deliver great performance at load, but also correct user experience and functionality. In production, with all the integrations there from your team, and from all third-party suppliers including Content Delivery Network partners, plug-in code partners (including social networks) and tracking codes. Not to mention the myriad of third-party programmatic advertisers, the true performance of the full, integrated app can be tested and measured. SOASTA was founded simultaneous with the public cloud, and they have always advocated for testing in production from the public cloud. This is where scale load testing is available at low cost through cloud service partners, including Amazon Web Services, Google Cloud Platform, Microsoft Azure, and others. When developers are building tests that run in development and through to production, and performance engineers are building tests that run in pre-prod, production, and in development, with automation executing these tests continuously, then the whole team can have confidence that there is enough testing to deliver the solution to market, avoiding the risk of missing serious defects while delivering great performance. Rod Cope, CTO of Rogue Wave So who owns this? In DevOps, everyone is responsible for testing, from the developer to QA to the IT director. This doesn’t mean more tests to reach some impossible-to-reach goal of “enough testing”; rather, embedding the tools, processes, and training across all teams to support rapidly shifting requirements, features and release cycles. QA is no longer the gatekeeper; they act as enablers for automated testing and reporting that needs little to no human intervention. Naturally, relevant standards and compliance come into play to assure both internal and external mandates are met. These are typically brought into the process early via user stories and the various acceptance criteria or definitions of done, and can be addressed with specificallym tuned checkers during static code analysis. Delivery dates, even in the Agile Age, are often immutable, so testing may simply reflect the amount of time or effort that’s been put into it, rather than the desired end state. Business decisions and market forces dictate when products are released. When does development alone get to specify a launch date? Rarely, if ever. Back to the fundamental question: There’s no way to determine the right amount of testing. But there are ways to ensure development teams have a consistent and realistic process, supporting tools that don’t slow it down, and a shared understanding of what’s expected. Tim Hinds, product marketing manager at Neotys On the other hand, if the app performance is critical to your business, you want to test scenarios that are as close to real life as possible, and use tools that can do this in an automatic way. Otherwise, you’re forced to make the compromise between speed of delivery and reliability of app performance. Alon Girmonsky, CEO of BlazeMeter The problem is that even with 100% test coverage you are only covering the predefined tests. In production, you are likely to find additional scenarios and user flows that the planned testing didn’t account for. These flows that real users travel may be the very operations that lead to unexpected system behavior. By testing these common user flows and scenarios on top of the 100% test coverage, you arrive at the 120% figure. Without the “What do users actually do in production?” component, you can’t be sure you are ready to deliver without surprises. See here for more information on the growth of Dev-Test-Ops, and here for a roundup of Dev-Test-Ops offerings. Companies may be shifting testing left, but lack of access to internal services as well as external services can delay testing and cause unnecessary bottlenecks. According to the Sogeti 2019 Continuous Testing report, test environments are one of the biggest bottlenecks to achieving continuous testing. The survey results reveal the inordinate amount of time that organizations spend on test environment management as well as some of the key challenges in this area. Time came up as a key issue when respondents were asked about – “test environment-related challenges that impeded efforts to Boost the software development lifecycle (SDLC).” Participants gave the highest weighting to “wait times and cost for environment provisioning” (36% of respondents) and “complexity of needed applications” (36%), followed by “inability to identify defects early in the testing process” (33%). RELATED CONTENT:

This is where service virtualization can come in. Service virtualization (SV) simulates or “mocks” unavailable systems by emulating their dynamic behavior, data, and performance. This means that teams can work in parallel for faster delivery. Mock services or service virtualization are critical for when the application or module you are developing and testing is dependent on the other services or systems regardless whether external or internal. Such dependencies could cause major testing bottlenecks, as they may not be easily available when you need them, or they may have constraints like costs or limited control over data it returns. Mock services remove these dependencies and also help to control the behavior of the dependencies by simulating the service using the endpoint provisioned by you – and this moves your testing to the next level. You can read this blog post on the benefits and concepts behind Mock services and service virtualization concept in general. The Sogeti report continues, “We have also seen a few positive developments in terms of the adoption of virtualization, containerization, and tool-based automation. These trends are likely to strengthen in the future as organizations realize that virtualization and containerization are absolutely necessary to meet the demands of Agile and DevOps on a limited budget. The next two to three years are also likely to see organizations opting for increased levels of automation, particularly for solutions that automatically tell them about the impact that changes in functional requirements will have on test cases.” Service virtualization shifts left Rather than waiting for the end of the testing cycle, and relying on service virtualization as a pre-production only tool, SV has become democratized, with developers creating mock environments for smaller unit tests, throughout the SDLC. Tools like WireMock and CodeSV can help developers to create mock services so they are not reliant on enterprise service virtualization support, and users can even integrate enterprise service virtualization capabilities with BlazeMeter, so that developers across all teams can create virtual services to test faster and more effectively. Sign up for our webinar here to learn more about service virtualization and how it can help you test faster, and with less bottlenecks in 2020. Content provided by SD Times and Broadcom. Listen to an example role play. - El mayor problema en mi ciudad es la basura en las calles. - ¿Y qué haces tú para ayudar con este problema? - Ayudo a limpiar los parques. - ¿Qué hiciste la semana pasada? - Viajé en bicicleta al colegio cada día. - ¿Te gustaría hacer algo diferente en el futuro? - Me gustaría ser parte de un grupo ecologista. - Me parece muy interesante. - ¿Qué hacéis en tu colegio? - En mi colegio apagamos las luces y los ordenadores al final del día. - The biggest issue in my city is the rubbish on the streets. - What do you do to help with this problem? - I help to clean the parks. - What did you do last week? - I travelled to school by bike every day. - Would you like to do something different in the future? - I would like to join an environmental group. - I find it very interesting. - What do you do in your school? - In my school they switch off the lights and the computers at the end of the day. The questions that follow are designed to make prospective students aware of the mathematics background required for those intending to take courses that are designated as Quantitative/Analytical (Q courses). The genuine test will cover the same concepts as this practice questions does, but the questions will be different. For more information about the expectations, read Q Assessment Topics. If you do not achieve a passing score on the genuine test, you will be required to enroll in and pass the course FAN X99: Foundations of Analytical and Quantitative Reasoning prior to taking any Q courses at SFU. You should be aware of the following conditions when you attempt this practice test:

| ||||||||

BEC download | BEC test Questions | BEC study | BEC resources | BEC teaching | BEC reality | BEC information search | BEC study help | BEC techniques | BEC test | | ||||||||

Killexams test Simulator Killexams Questions and Answers Killexams Exams List Search Exams |

BEC Reviews by Customers

Customer Reviews help to evaluate the exam performance in real test. Here all the reviews, reputation, success stories and ripoff reports provided.

100% Valid and Up to Date BEC Exam Questions

We hereby announce with the collaboration of world's leader in Certification Exam Dumps and Real Exam Questions with Practice Tests that, we offer Real Exam Questions of thousands of Certification Exams Free PDF with up to date VCE exam simulator Software.